Key Takeaways

✓ Most money mistakes are not math problems — they are behavior problems driven by emotion, habit, and belief

✓ Understanding why you make a mistake is the only way to permanently stop making it

✓ The financial patterns you repeat today were usually formed long before you had any money

✓ Awareness without a system to replace the behavior changes nothing

✓ Small consistent financial decisions compound over time exactly the same way small consistent mistakes do

You have told yourself you were going to stop overspending. You made a budget. You committed to saving more. And then three weeks later you were right back where you started, wondering what happened.

If this sounds familiar, you are not bad with money. You are human. The same money mistakes repeat themselves not because people lack knowledge but because behavior is harder to change than information is to learn. This guide explains the real reasons behind the financial patterns that keep showing up in your life — and what it actually takes to break them.

The Real Reason Most Money Mistakes Repeat

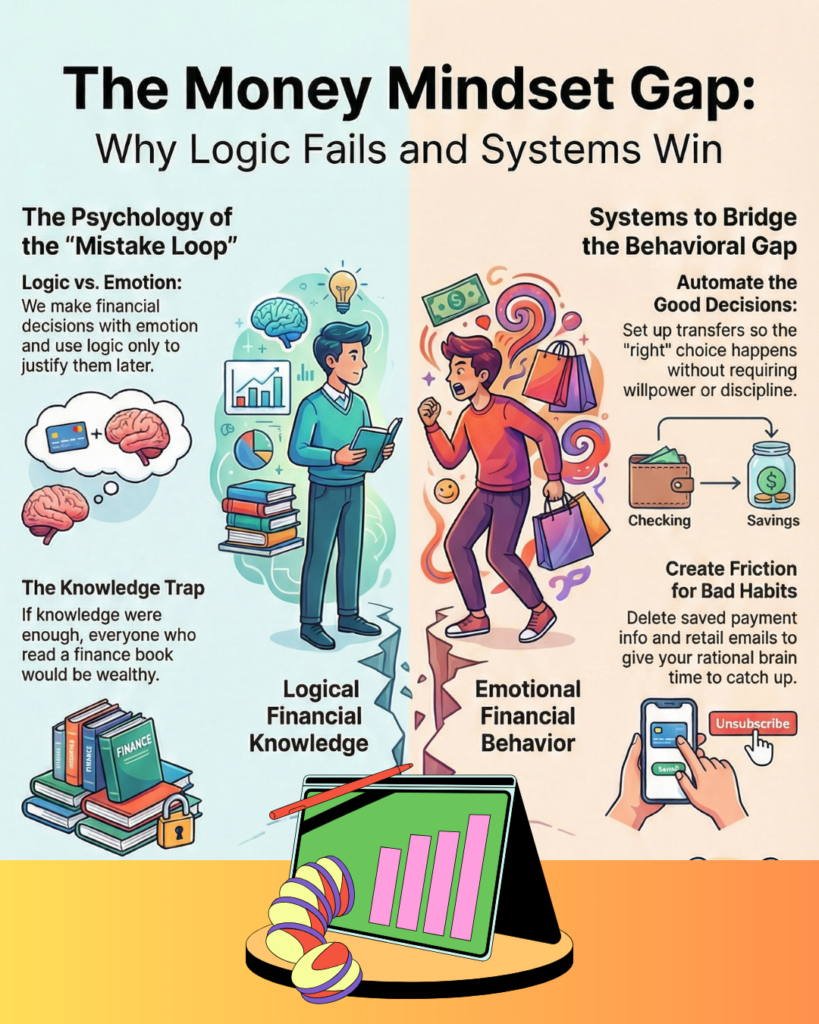

Personal finance education focuses almost entirely on the mechanics of money — how to budget, how to invest, how compound interest works. What it rarely addresses is the psychological dimension of financial behavior. And that is where most people actually struggle.

Research in behavioral economics consistently shows that people do not make financial decisions primarily with logic. They make them with emotion and then use logic to justify what they already decided. Fear, insecurity, optimism bias, peer pressure, and childhood money experiences all drive financial behavior more powerfully than any spreadsheet ever will.

The Hard Truth

If knowledge were enough to change financial behavior, everyone who has read a personal finance book would be financially secure. Knowledge is necessary but it is not sufficient. Behavior change requires understanding the specific emotional driver behind the specific mistake.

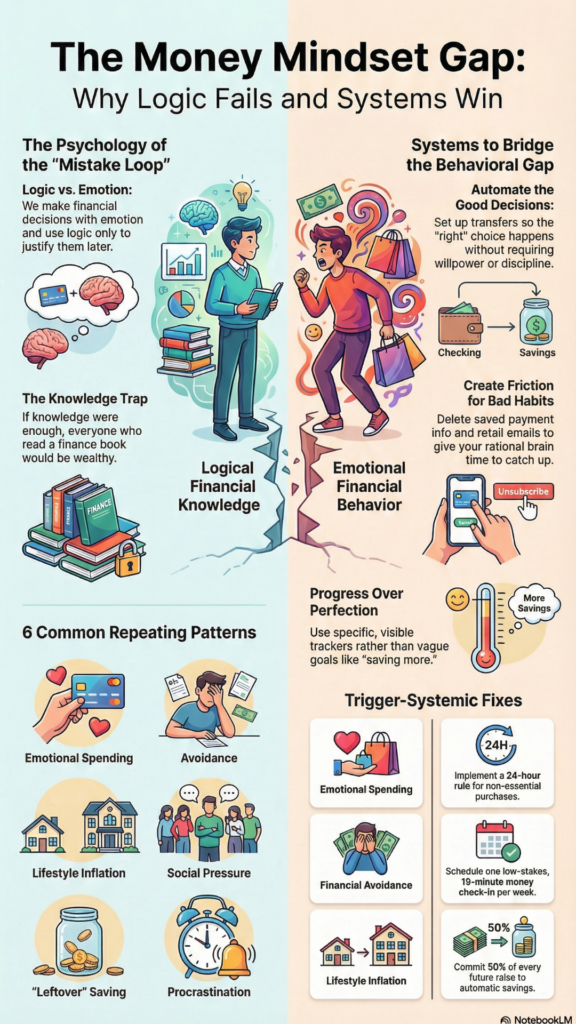

The 6 Most Common Repeating Money Mistakes

1. Spending to Feel Better in the Moment

Emotional spending is one of the most common and least discussed financial patterns. Stress, boredom, loneliness, and even celebration trigger spending as a coping mechanism. The purchase feels good for a brief window. Then the financial guilt sets in. Then the stress that triggered the spending returns — often worse. Then the cycle repeats.

How to break it:

Identify your specific emotional triggers before you are in them. Create a 24-hour rule for non-essential purchases over a set amount. Find a non-financial replacement behavior for the emotional state that triggers spending.

2. Avoiding Money Altogether

Many people who struggle financially are not reckless spenders. They are avoiders. They do not open bank statements. They do not look at their account balance. They do not review their bills. The avoidance feels protective in the short term but the financial problems it allows to grow are far more damaging than the discomfort of facing them early.

How to break it:

Schedule one 15-minute money check-in per week. Make it low-stakes — you are just looking, not solving everything at once. Consistent small exposures reduce the anxiety that drives avoidance over time.

3. Lifestyle Inflation That Outpaces Income Growth

Every time income increases, spending increases to match it — sometimes beyond it. A raise that should have accelerated savings instead just funds a more expensive lifestyle. This is lifestyle inflation, and it is one of the most consistent wealth-building killers across all income levels. People earning $100,000 per year often have no more financial cushion than people earning $50,000 because their expenses scaled exactly with their income.

How to break it:

Commit to saving or investing at least 50 percent of every raise or income increase before adjusting your lifestyle. Automate the savings so the money is moved before you have a chance to spend it.

4. Financial Decision Making Under Social Pressure

Buying things to match what peers have, attending expensive events out of social obligation, lending money you cannot afford to lose, or making major financial decisions to avoid conflict — all of these are forms of social financial pressure. They rarely show up in budgeting apps but they quietly drain wealth over time.

How to break it:

Get clear on your own financial values and goals first. When a social spending pressure arises, measure it against your goals — not against what others are doing or what feels expected.

5. Treating Savings as What Is Left Over

Most people save whatever is left at the end of the month after spending. The problem is that spending expands to fill available money. There is almost never anything left over. Saving has to come first — before spending, before discretionary decisions, before anything else. Pay yourself first is not a cliche. It is the only savings system that actually works consistently.

How to break it:

Set up an automatic transfer to savings on the same day your paycheck arrives. Treat it like a bill you cannot skip. Start with any amount — even $25 per paycheck. The habit matters more than the amount when you are starting.

6. Waiting for the “Right Time” to Start

When the debt is paid off. When I get that raise. When the kids are grown. When things settle down. The right time to start saving, investing, and building financial security is always some version of not right now. Meanwhile compounding works against you every month you delay. The people who build wealth are not the ones who waited for perfect conditions — they are the ones who started imperfectly and kept going.

How to break it:

Identify the specific condition you are waiting for and ask yourself honestly whether it will actually change your financial behavior when it arrives. Usually it will not. Start now with whatever you have.

The System That Actually Changes Financial Behavior

Awareness alone does not change behavior. You can know exactly why you overspend and still do it. What actually works is replacing the behavior with a system that does not require willpower or perfect emotional regulation in the moment.

Automate the good decisions. Savings transfers, bill payments, and investment contributions that happen automatically do not require you to make the right choice every month. They happen whether your mood is good or bad, whether you feel disciplined or not.

Create friction for the bad decisions. Unsubscribe from retail emails. Delete saved payment information from shopping sites. Put a 24-hour waiting period on purchases above a set amount. Friction does not eliminate the desire to spend — it gives the rational part of your brain time to catch up with the emotional part.

Track progress toward something specific. Vague financial goals — “save more money,” “spend less” — do not motivate behavior change. Specific visible goals do. A savings tracker on your wall showing progress toward a $5,000 emergency fund works better than a mental commitment to be more responsible.

Connect your money decisions to your real life goals. Abstract financial discipline is hard to sustain. Saving for your child’s education, your retirement, or your family’s security is much easier to sustain because it connects the sacrifice to something that actually matters to you.

James’s Take

“In my years working with families on financial decisions, the pattern I see most consistently is not ignorance about how money works. It is the gap between what people know they should do and what they actually do when the emotional pressure is on. The families who make real progress are the ones who stop relying on willpower and build systems that make the right financial behavior the default. Automation is not a shortcut. It is the strategy.”

James A. Sabb, Financial Educator and CEO, Sabb Media International LLC

Frequently Asked Questions

Why do I keep spending money even when I know I should not?

Because the decision to spend usually happens in an emotional state where the immediate reward feels more real than the future consequence. This is not a moral failure — it is how human brains work. The solution is not more willpower but better systems that remove the decision from the emotional moment entirely.

How do childhood experiences affect adult financial behavior?

The financial patterns, beliefs, and emotional associations you grew up with form the foundation of your adult relationship with money. If money was scarce, stressful, or never discussed growing up, those early experiences shape how you feel and behave around money as an adult — often in ways you are not fully aware of. Recognizing these patterns is the first step to changing them.

Is budgeting really the answer to financial problems?

A budget is a tool, not a solution. Many people create budgets and abandon them within weeks because the budget addresses the mechanics of spending without addressing the emotional drivers. A budget works best when it is simple, realistic, and connected to goals that genuinely motivate you. The most complicated budget you will not follow is worse than the simplest one you will.

What is the fastest way to change a bad financial habit?

Identify the specific trigger, the specific behavior, and the specific reward the behavior provides. Then find a replacement behavior that satisfies the same emotional need without the financial cost. Trying to eliminate a behavior without replacing the reward it provides almost never works long term.

How long does it take to build a new financial habit?

Research suggests that habit formation takes anywhere from 21 to 66 days depending on the complexity of the behavior and the individual. Financial habits at the simpler end — like checking your bank balance weekly — tend to form faster. More complex behaviors like consistently saving a percentage of income can take two to three months of intentional repetition before they feel automatic.

Continue Learning

→Financial Planning Explained for Everyday People

→How to Build Household Wealth: A Practical No-Fluff Guide

→What the Banks Won’t Tell You About Personal Finance

→How Insurance Fits Into Your Financial Plan

Want to Keep Learning?

Explore plain-language guides on insurance, financial planning, investing, and consumer protection, all in one place.

Everything on SabbMedia.com is written and reviewed by James A. Sabb, a consultant with over 30 years of experience in regulated industries.

Written and Reviewed by James A. Sabb

Consultant and Advisor · 30+ Years Experience · Health Insurance Advisory Since 2015 · CEO, Sabb Media International LLC · Pompano Beach, FL

James A. Sabb has spent over three decades in regulated industries, including 10 plus years advising individuals and families on financial and insurance decisions within federally regulated environments. He founded SabbMedia.com to bring that inside expertise to everyday people. No sales pressure, no jargon, just clarity.

Disclaimer: The content on this page is intended for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Sabb Media International LLC is not a licensed financial advisor or insurance broker. James A. Sabb provides consultative and educational guidance only. Always consult a qualified, licensed professional before making any financial or insurance decisions.