How to Choose the Right Insurance Policy: A Complete Step-by-Step Guide

Key Takeaways

✓ The right insurance policy is not the cheapest one — it is the one that actually covers your biggest risks

✓ Start by identifying what you need to protect before comparing any policies

✓ Coverage limits matter more than premiums — know your worst-case scenario first

✓ Always read the exclusions — what a policy does not cover is just as important as what it does

✓ Shopping multiple insurers for the same coverage can save hundreds of dollars annually

Choosing an insurance policy can feel overwhelming. There are dozens of options, confusing terminology, and no shortage of salespeople telling you their product is the best one. But the process of choosing the right policy is actually straightforward when you know what to look for.

This guide walks you through a simple step-by-step process for evaluating any insurance policy — health, auto, life, or property — so you can make an informed decision with confidence instead of guesswork.

Step 1 — Identify What You Are Actually Protecting

Before you look at a single policy, get clear on what you need to protect. This sounds obvious but most people skip it and go straight to comparing prices. That is how you end up with a policy that looks affordable on paper but leaves you exposed when something happens.

1

List your assets and income

What do you own? What do you earn? Who depends on that income? Your home, car, savings, and the people who rely on you financially are all things insurance is designed to protect.

2

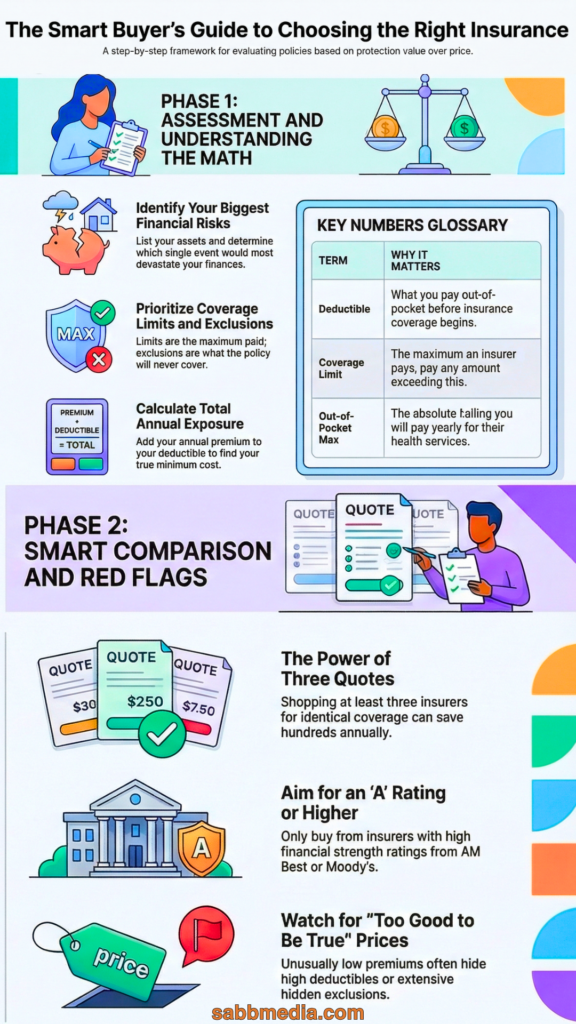

Identify your biggest financial risks

What single event could most devastate your finances? A medical emergency? A car accident that injures someone? Losing your home to fire? Your insurance choices should be driven by your biggest risks, not your smallest ones.

3

Define your budget for premiums

Know what you can comfortably pay every month before you start comparing. This prevents you from buying more than you need or underbuying because you are shocked by prices.

Step 2 — Understand the Key Numbers Before Comparing Policies

Every insurance policy has a set of numbers that determine what you pay and what you get. Understanding these before comparing policies is what separates informed buyers from people who get surprised after a claim.

Premium

Your monthly or annual cost for coverage. The most visible number but not the most important one.

Deductible

What you pay out of pocket before coverage begins. A higher deductible lowers your premium but means more out of pocket when you file a claim. Only choose a high deductible if you have that amount readily available.

Coverage Limits

The maximum your insurer will pay for a covered loss. This is the number most people underestimate. If a claim exceeds your limit, you pay the difference personally. Always ask yourself what the worst-case scenario looks like and whether your limit covers it.

Exclusions

What the policy does not cover. This is the most important section of any policy document. Always read the exclusions before signing. Many people discover their biggest risk is excluded only after they file a claim.

Out-of-Pocket Maximum (Health Insurance)

The most you will pay in a year before your insurer covers 100 percent. This is your financial ceiling and the most protective number in a health insurance policy. Always compare this across plans.

Step 3 — Compare Policies the Right Way

Once you know what you need and understand the key numbers, comparing policies becomes straightforward. Here is what to look at side by side.

Compare total annual cost not just premium. Add your annual premium to your deductible. That is your minimum annual exposure. A low premium with a high deductible often costs more total than a moderate premium with a lower deductible if you actually use the coverage.

Match coverage limits to your real risk. For liability coverage, ask yourself what it would cost if you caused the worst possible accident or someone filed a serious lawsuit. State minimums are rarely sufficient for this.

Check the insurer’s financial strength rating. An insurer that cannot pay claims is worthless. Check ratings from AM Best, Moody’s, or Standard and Poor’s. Look for an A rating or higher before buying from any company.

Get at least three quotes. The same coverage from different insurers can vary by hundreds of dollars per year. Shopping multiple companies for identical coverage is the fastest way to reduce your premium without reducing your protection.

The National Association of Insurance Commissioners (NAIC) offers free tools and guides to help consumers compare insurance policies, understand coverage terms, and verify that insurers are licensed to operate in their state.

Step 4 — Watch Out for These Red Flags

⚠

Pressure to decide immediately

No legitimate insurer requires you to buy on the spot. Any pressure to sign before you have had time to read and compare is a red flag.

⚠

Premiums that seem too good to be true

Unusually low premiums usually mean high deductibles, low coverage limits, or a long list of exclusions. Always ask why the price is so much lower than competitors before assuming it is a good deal.

⚠

Unclear or confusing exclusions

If you cannot get a clear answer about what the policy does not cover, do not buy it. A trustworthy insurer can explain their exclusions in plain language.

⚠

No license or credentials you can verify

Any agent selling insurance must be licensed in your state. You can verify an agent’s license through your state’s department of insurance website. Always check before giving anyone your personal or financial information.

James’s Take

“The single most important thing I tell anyone choosing an insurance policy is this: read the exclusions before you read the price. I have seen families discover that their biggest risk was excluded from their policy only after they needed to file a claim. By then it is too late. Spend ten minutes with the exclusions section before you sign anything. That ten minutes can save you from a financial disaster.”

James A. Sabb, Insurance Advisor and CEO, Sabb Media International LLC

Frequently Asked Questions

Should I use an independent agent or go directly to an insurer?

An independent agent can shop multiple insurers on your behalf and help you compare options objectively. A captive agent works for one company only. For most consumers, working with an independent agent saves time and often results in better coverage at a lower price. Either way, verify they are licensed in your state.

How do I know if I have enough coverage?

Ask yourself one question: if the worst thing that could realistically happen actually happened, would my coverage be enough to keep my family financially stable? If the answer is no, you need more coverage. If yes, you may be properly covered or even overinsured on some policies.

Can I bundle policies to save money?

Yes. Most insurers offer multi-policy discounts when you bundle auto and homeowners or renters insurance with the same company. Bundling can save 5 to 25 percent on your premiums. However, always compare the bundled price against separate policies from different insurers to make sure you are actually getting a deal.

What is a policy declaration page?

The declaration page is the summary page of your insurance policy. It shows your coverage types, limits, deductibles, premium, policy period, and named insureds. It is the first page you should look at when reviewing any policy. Keep a copy somewhere you can access it quickly after an accident or loss.

How often should I shop my insurance rates?

At minimum every one to two years at renewal time. Rates change constantly. Your circumstances change. A clean driving record that builds up over time, a credit score improvement, or moving to a different zip code can all qualify you for lower rates. Loyalty to one insurer almost never results in the best price.

Continue Learning

→Insurance and Risk Management: The Complete Guide for Families

→Common Insurance Mistakes to Avoid: A Complete Guide

→Understanding Insurance Premiums: What You Pay and Why

→What Does Insurance Actually Cover? The Complete Guide

Want to Keep Learning?

Explore plain-language guides on insurance, financial planning, investing, and consumer protection, all in one place.

Everything on SabbMedia.com is written and reviewed by James A. Sabb, a consultant with over 30 years of experience in regulated industries.

Written and Reviewed by James A. Sabb

Consultant and Advisor · 30+ Years Experience · Health Insurance Advisory Since 2015 · CEO, Sabb Media International LLC · Pompano Beach, FL

James A. Sabb has spent over three decades in regulated industries, including 10 plus years advising individuals and families on insurance decisions within federally regulated environments. He founded SabbMedia.com to bring that inside expertise to everyday people. No sales pressure, no jargon, just clarity.

Disclaimer: The content on this page is intended for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Sabb Media International LLC is not a licensed financial advisor or insurance broker. James A. Sabb provides consultative and educational guidance only. Always consult a qualified, licensed professional before making any financial or insurance decisions.