Key Takeaways

✓ Liability coverage pays for damage you cause to others — it does not cover your own vehicle

✓ Full coverage combines liability, collision, and comprehensive — it protects your car too

✓ Every state requires minimum liability coverage — full coverage is optional but often worth it

✓ If your car is financed or leased, your lender almost certainly requires full coverage

✓ The right choice depends on your car’s value, your savings, and your risk tolerance

You’re standing at the insurance counter or clicking through an online quote, and the question hits you: do I need liability only, or should I get full coverage? It’s one of the most common decisions drivers face — and one of the most misunderstood. Get it wrong and you could be paying for coverage you don’t need, or worse, find yourself without protection when something goes wrong.

This guide breaks down exactly what each type covers, what it doesn’t, and how to figure out which one fits your situation.

What Liability Auto Insurance Actually Covers

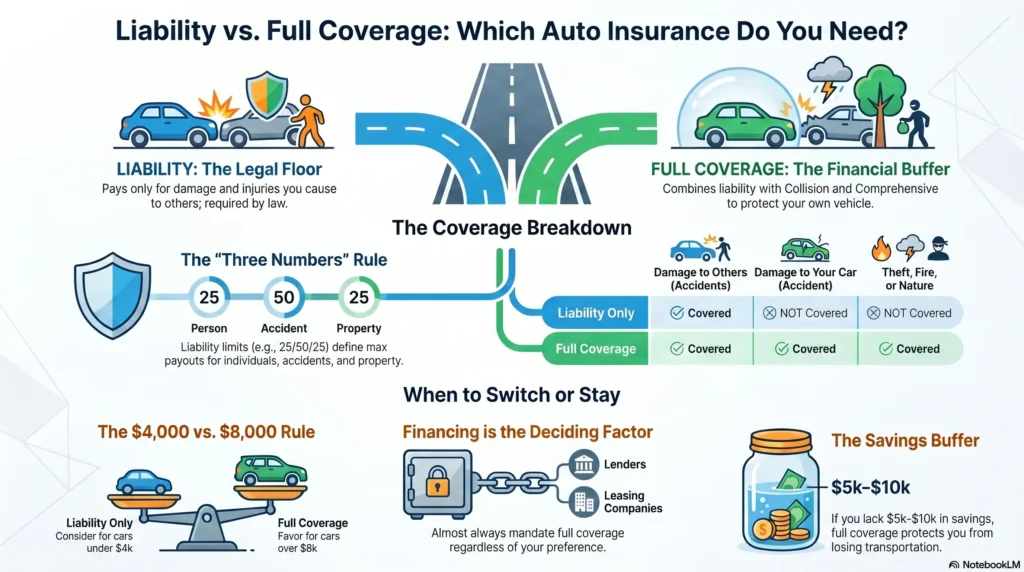

Liability insurance covers the damage you cause to other people when you’re at fault in an accident. That includes the other driver’s vehicle repairs, their medical bills, and in serious cases, legal costs if they sue you.

What it does not cover is your own vehicle. If you cause an accident and your car is totaled, liability insurance pays nothing toward replacing it. You absorb that loss entirely out of pocket.

Liability coverage is expressed as three numbers — for example, 25/50/25. The first number ($25,000) is the maximum paid per injured person. The second ($50,000) is the maximum per accident. The third ($25,000) covers property damage. Every state sets its own minimum required limits. The National Association of Insurance Commissioners (NAIC) maintains a full breakdown of state requirements if you want to verify your state’s minimums.

What Full Coverage Auto Insurance Actually Covers

“Full coverage” isn’t a single product — it’s a combination of three types of coverage bundled together. Understanding each piece matters.

Liability

Same as described above — covers damage and injuries you cause to others. Required by law in almost every state.

Collision

Covers damage to your own vehicle when you hit another car or object — regardless of fault. If you rear-end someone or slide into a guardrail, collision pays to repair or replace your car minus your deductible.

Comprehensive

Covers damage from events that aren’t collisions — theft, fire, flooding, hail, a tree falling on your car, or hitting an animal. If a hurricane rolls through Florida and destroys your vehicle, comprehensive is what pays.

Together these three give you protection on both sides of an accident — what you cause and what happens to you. That’s the core difference between liability only and full coverage.

Liability vs Full Coverage: When Each One Makes Sense

The right choice depends on three factors — your car’s current market value, what you have in savings, and whether your vehicle is financed.

→

Your car is worth less than $4,000

Liability-only may make financial sense. If the payout on a totaled vehicle barely exceeds the annual cost of full coverage, the math tips toward dropping collision and comprehensive.

→

Your car is worth more than $8,000

Full coverage is worth considering. The potential loss exposure is significant enough that the premium cost is usually justified — especially if replacing the vehicle would strain your budget.

→

Your car is financed or leased

Full coverage is almost certainly required by your lender. This isn’t optional — check your loan or lease agreement. Dropping coverage on a financed vehicle violates the terms and can result in the lender forcing coverage on your behalf at a far higher cost.

→

You don’t have $5,000–$10,000 in accessible savings

Full coverage acts as a financial buffer. If an accident totals your car and you don’t have savings to replace it, liability-only leaves you without transportation. The premium you pay for full coverage is essentially funding that buffer.

For a broader look at how auto insurance fits into your overall financial protection plan, see our Insurance & Risk Management guide and our overview of Auto Insurance basics.

Common Mistakes to Avoid

These are the patterns that end up costing drivers the most — not dramatic mistakes, just quiet ones made at renewal time.

Carrying state minimum liability limits: State minimums were set years ago and often don’t reflect the real cost of a serious accident. A $25,000 bodily injury limit disappears fast in a multi-person accident. Higher limits are available and usually cost less than people expect.

Choosing a deductible you can’t actually pay: Full coverage includes a deductible — typically $500 to $1,000 — that you pay before insurance kicks in. Choosing a $1,500 deductible to lower your premium only helps if you have $1,500 available when something goes wrong.

Not updating coverage as your car ages: A car you bought new five years ago with full coverage may no longer justify that cost today. Review your coverage annually as the vehicle’s value decreases.

Frequently Asked Questions

Is full coverage required by law?

No — state law requires liability coverage, not full coverage. Full coverage becomes effectively required when your lender or leasing company mandates it as a condition of your financing agreement. Once your vehicle is paid off, full coverage is your choice to make.

How much more does full coverage cost than liability only?

The difference varies significantly based on your vehicle, driving history, location, and the deductible you choose. For many drivers the difference runs between $50 and $150 per month. The key question is whether that monthly cost is worth the protection against a total loss — which depends entirely on your vehicle’s value and your savings cushion.

What happens if I only have liability and someone hits me?

If the other driver is at fault and carries insurance, their liability coverage should pay for your vehicle damage. The complication arises when the at-fault driver is uninsured or underinsured. Without uninsured motorist coverage — which you can add separately — you may have limited recourse for your own vehicle damage in that situation.

Can I switch from full coverage to liability only at any time?

Generally yes — unless your vehicle is financed or leased, in which case you cannot drop below the coverage your lender requires. If your car is paid off, you can adjust your coverage at any point during your policy term. Most insurers will prorate any refund for unused premium if you reduce coverage mid-term.

The Bottom Line

Liability coverage is the legal floor. Full coverage is the financial buffer. The decision between them comes down to what your car is worth, what you have in savings, and whether a total loss would set you back financially. Neither choice is universally right — it depends on your specific situation evaluated honestly.

Review your coverage every year at renewal. Your car’s value changes, your financial situation changes, and your coverage should reflect that.

Want to understand your full insurance picture?

Explore plain-language guides on every type of coverage — health, auto, life, and property.

Written & Reviewed by James A. Sabb

30+ Years Experience | Financial Education Consultant | CEO, Sabb Media International LLC | Pompano Beach, FL

James A. Sabb has spent over three decades in regulated industries, including years advising individuals and families on insurance and financial protection decisions. He founded SabbMedia.com to bring that expertise to everyday people — no sales pressure, no jargon, just clarity.

Disclaimer: The content on this page is intended for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Sabb Media International LLC is not a licensed financial advisor or insurance broker. James A. Sabb provides consultative and educational guidance only. Always consult a qualified, licensed professional before making any financial or insurance decisions.