⚡ Key Takeaways

✓ You can start investing with $100 or less — many platforms require $0 minimum

✓ Starting today with $100 beats waiting until you have $1,000 next year

✓ Index funds and ETFs are the best starting point — low cost, instant diversification

✓ $100/month at 8% average return grows to over $17,000 in 10 years

✓ Starting small and imperfect beats waiting for the “perfect” moment

Let’s be honest — if you’ve Googled “how to start investing,” you’ve probably landed on articles that make it sound like you need thousands of dollars and a stockbroker named Geoffrey before you can get started. That’s simply not true anymore, and it hasn’t been true for years.

The reality? You can start investing with $100 today. Not “sort of investing.” Real, actual investing — in the same companies and funds that wealthy people own — starting right now with whatever you have.

This guide is written for real people with real budgets. We’ll walk through exactly where to put that first $100, what to expect, and how to grow it into something meaningful. No jargon. No shame. Let’s go.

Why $100 Is Genuinely Enough to Start Investing

A decade ago, most brokerage accounts required minimums of $500–$2,500 to open. That’s changed completely. Today, thanks to fractional shares — the ability to buy a slice of a stock rather than a whole share — you can own a piece of Amazon or a diversified index fund for as little as $1.

💭 You Might Be Thinking…

“But $100 is nothing. What’s even the point?” — The point is habit, momentum, and compound interest. The person who starts with $100 today and adds $50 a month will lap the person who waits until they “have enough.” Every single time.

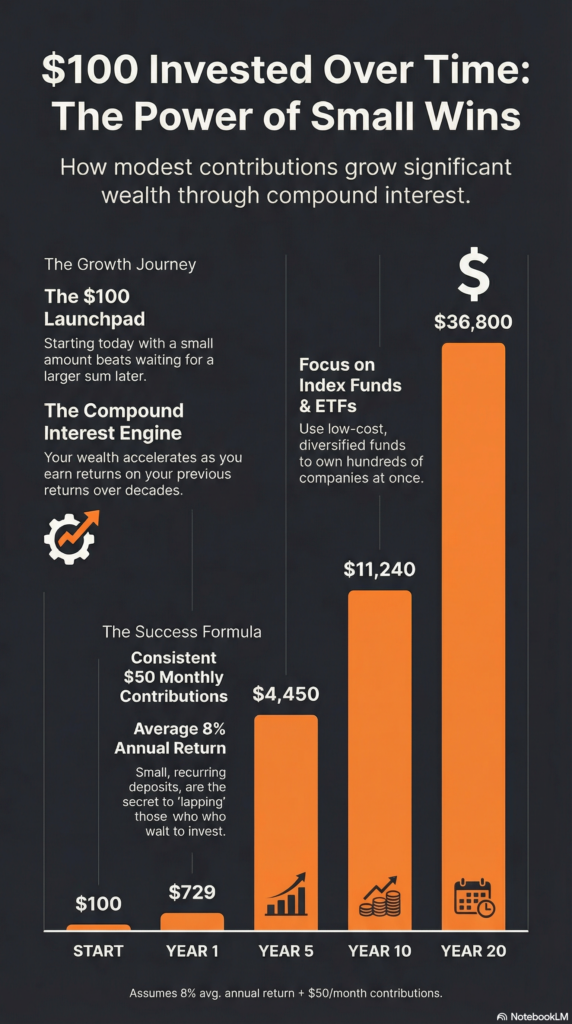

Here’s what the math looks like when you invest $100 and add just $50 every month at a historical average return of 8% per year:

Start

$100

Day 1

Year 1

$729

$50/mo added

Year 5

$4,450

Solid foundation

Year 10

$11,240

Real wealth building

Year 20

$36,800

The magic of time

*Assumes 8% avg. annual return, $50/month contributions. For illustration only — actual returns vary.

The concept at work here is compound interest — earning returns on your returns. It rewards people who start early far more than people who start with large amounts later. 📖 New to investing? Read our Investing Basics for Beginners guide first →

Before You Invest: Two Things to Check Off First

Investing is powerful, but it shouldn’t come at the expense of your financial safety net. Before you put money into the market, make sure you have these covered:

🔴 High-interest debt: If you’re carrying credit card debt above 10% interest, pay that down first. No investment reliably outpaces a 22% APR credit card.

🔴 A starter emergency fund: Even $500–$1,000 in a savings account prevents you from being forced to sell investments at the wrong time. Build yours first →

💡 Quick Tip

You don’t need a full 3–6 month emergency fund before investing. Many experts suggest building a $1,000 cushion first, then starting to invest simultaneously. The key is getting started — not waiting for perfect conditions.

Where to Invest $100: 6 Best Options for Beginners

Here are the six best options, ranked from most beginner-friendly to slightly more advanced.

1. Index Funds & ETFs — The Gold Standard for Beginners

An index fund is a collection of stocks designed to mirror a market index — like the S&P 500. When you buy one share, you own tiny pieces of Apple, Microsoft, Amazon, and 497 other companies at once. An ETF works similarly but trades like a stock. See our Index Funds vs. ETFs guide →

Popular examples: FZROX (Fidelity Zero Total Market), VOO (Vanguard S&P 500 ETF), SCHB (Schwab US Broad Market ETF)

• Instant diversification

• Low or zero fees

• Historically ~7–10% annual returns

• No research required

• Returns not guaranteed

• Market will dip — stay calm

• Boring (that’s actually a feature)

2. Robo-Advisors — Investing on Autopilot

A robo-advisor builds and manages a diversified portfolio for you based on your goals and risk tolerance. You answer a few questions, deposit money, and it handles everything — automatically rebalancing and reinvesting dividends.

Popular platforms: Betterment, Wealthfront, SoFi Automated Investing, Fidelity Go

• Totally hands-off

• Auto rebalances

• Low minimums ($0–$10)

• Tax-loss harvesting on some

• 0.25–0.50% annual fee

• Less control over holdings

• Fee compounds against you over time

3. Micro-Investing Apps — Start with Spare Change

Apps like Acorns, Stash, and Public let you invest very small amounts — even automatically rounding up your purchases and investing the difference. Spent $4.60 on coffee? Acorns rounds to $5.00 and invests the $0.40.

Best for: People who struggle to save and want investing to happen automatically.

• Extremely low friction

• Great for building the habit

• Built-in learning resources

• $1–$5/mo fee is high on small balances

• Round-ups alone grow very slowly

• Not a standalone strategy

4. High-Yield Savings Account — Safe & Liquid

Not technically “investing,” but a high-yield savings account at an online bank currently earns 4–5% APY with zero risk (FDIC insured). It massively outperforms a traditional savings account at 0.01% APY and is perfect for short-term goals.

• Zero risk — FDIC insured

• 4–5% returns right now

• Fully liquid, withdraw anytime

• Rates will drop over time

• Won’t build long-term wealth alone

• Inflation can outpace returns

5. Your Employer’s 401(k) — The Best “Investment” You May Be Ignoring

If your employer offers a 401(k) match and you’re not taking full advantage of it, fix that first. A 100% employer match is a guaranteed 100% instant return — nothing in the market comes close to that.

• Free money from employer

• Tax-advantaged growth

• Reduces taxable income

• Locked until age 59½

• Limited investment options

• Not available to all workers

6. Fractional Shares in Individual Stocks — For the Curious

With fractional shares, you can buy $5 worth of Amazon or $10 worth of Tesla. Platforms like Fidelity, Schwab, Robinhood, and M1 Finance all offer this. Best used once you already have a core index fund portfolio established.

• Buy any stock from $1

• Engaging and educational

• Own companies you love

• Riskier than index funds

• Requires research

• Easy to overtrade emotionally

Best Investment Apps for Beginners: Side-by-Side Comparison

Here’s a look at the most popular platforms for beginners starting small. See our full Best Investment Apps 2026 review →

| Platform | Minimum | Type | Index Funds | Fractional Shares | IRA Account | Annual Fee |

|---|---|---|---|---|---|---|

| Fidelity Best Overall | $0 | Brokerage | ✓ | ✓ | ✓ | $0 |

| Charles Schwab | $0 | Brokerage | ✓ | ✓ | ✓ | $0 |

| Betterment Best Robo | $0 | Robo-Advisor | ✓ | ✗ | ✓ | 0.25%/yr |

| Acorns | $0 | Micro-Invest | ✓ | ✗ | ✓ | $3/mo |

| M1 Finance | $100 | Brokerage | ✓ | ✓ | ✓ | $0* |

| Public | $0 | Brokerage | ✓ | ✓ | ✗ | $0 |

Step-by-Step: How to Make Your First Investment with $100

Step 1

📋 Open a Brokerage or IRA Account (10 minutes)

Go to Fidelity.com, Schwab.com, or your chosen platform and click “Open an Account.” You’ll need your Social Security number, a government ID, and your bank account info. For most beginners, a regular brokerage account or a Roth IRA (if you have earned income) is the right starting point.

Step 2

💳 Link Your Bank Account and Deposit $100

Transfer $100 from your checking account. It takes 1–3 business days. Some platforms like Fidelity allow immediate trading even before the transfer fully clears. You’ll need your bank’s routing and account numbers, found on a check or in your banking app.

Step 3

🔍 Search for Your First Investment

In the search bar, type the ticker symbol of what you want to buy. For a great diversified start, consider: FZROX (Fidelity Zero Total Market — 0% expense ratio), VTI (Vanguard Total Stock Market ETF), or SPY (S&P 500 ETF). These are simple, diversified, and proven over decades.

Step 4

🛒 Place Your First Buy Order

Click “Trade” or “Buy.” Select dollar amount (not shares) to invest exactly $100. Choose “Market Order.” Review the order summary, take a breath, and click “Place Order.” You are now officially an investor.

Step 5 — Most Important

🔁 Set Up Automatic Monthly Contributions

Go to your account settings and set up automatic recurring investments — even $25 or $50/month. This is called dollar-cost averaging, and it means you automatically buy more shares when prices are low and fewer when they’re high. Set it, forget it, and let time do the work.

⚠️ Common Mistake: Don’t Panic-Sell

After you invest, the market will go down at some point. The #1 mistake beginners make is seeing their $100 dip to $88 and selling in a panic. That locks in the loss. Investors who hold through downturns and keep contributing almost always come out far ahead of those who sell.

What to Expect: Realistic Returns and Timeframes

Let’s set honest expectations. Investing is not a get-rich-quick scheme — and any website that implies otherwise is misleading you.

Short term (0–2 years): Your $100 could be worth more or less. Markets fluctuate. Don’t invest money you’ll need within two years.

Medium term (3–7 years): Historical S&P 500 returns average ~7–10% annually. Your $100 could realistically become $130–$200 with no additional contributions.

Long term (10–30 years): This is where the magic happens. At 8% average return, $100 becomes ~$216 in 10 years. Add $50/month contributions and you’re looking at $11,000+.

💭 You Might Be Thinking…

“What if the market crashes right after I invest?” — It might! That’s why you invest money you won’t need for at least 3–5 years. Every major crash in history — 2008, 2020, 2022 — was followed by a full recovery and new highs. The investors who got hurt are the ones who sold. The ones who stayed invested made more money than before the crash.

6 Common Mistakes Beginners Make with Small Investments

1

There is no perfect time. Every day you wait, you lose compounding. The market is always “uncertain” — that’s just what markets are.

2

A 1% annual fee sounds tiny — but on a $50,000 portfolio over 30 years it costs you over $100,000 in lost growth. Stick to index funds with expense ratios below 0.20%.

3

One bad earnings report and you’re down 30%. Index funds give you 500+ companies for the price of one. That’s diversification, and it’s your best defense against catastrophic loss.

4

Short-term price swings are noise. Constant checking leads to emotional decisions. Check monthly at most — the more you check, the more tempted you’ll be to react.

5

A market drop is a sale on stocks. Your regular contributions buy more shares when prices are lower. Keep going — this is how dollar-cost averaging works in your favor.

6

If an unexpected expense forces you to sell investments at the wrong moment, you could lock in a loss. Keep at least $500–$1,000 liquid before investing.

Frequently Asked Questions

Is $100 really enough to start investing?

Absolutely. Thanks to fractional shares and zero-minimum platforms, you can invest any dollar amount today. The psychological value of starting with $100 is enormous — it makes you an investor, not just someone who “plans to invest someday.”

What’s the safest investment for a beginner?

A broad market index fund — like one tracking the S&P 500 or Total US Stock Market — offers the best combination of safety through diversification, historically strong returns, and very low costs. It’s not risk-free, but it’s well-diversified and time-tested over 100+ years of market history.

Should I invest in a Roth IRA or a regular brokerage account?

If you have earned income, a Roth IRA is usually better for beginners. Your contributions are made with after-tax dollars, but all growth is completely tax-free. The 2025 limit is $7,000/year. If you might need the money before retirement, use a regular brokerage account — it’s more flexible.

What if I lose money?

In the short term, your investment will go down at some point — that’s how markets work. The question is whether you sell (locking in the loss) or hold (giving it time to recover). Investors who held through the 2008 crash and the 2020 COVID drop all fully recovered and went on to make significant gains.

Are micro-investing apps like Acorns worth it?

They’re great for building the habit and getting started. But watch the fees: Acorns charges $3/month. On a $100 balance that’s a 36% annual fee. Once your balance grows to $1,000+, the fee becomes just 0.36% — much more reasonable. Use micro-apps to build the habit, then graduate to a free platform.

How is investing different from saving?

Saving protects your principal with near-zero risk, but growth is minimal — even high-yield accounts max out around 4–5%. Investing accepts short-term risk in exchange for significantly higher long-term growth. The S&P 500 has returned ~10% annually before inflation — roughly doubling your money every 7–10 years.

How long until I see real growth?

You’ll see small fluctuations in the first few months. Meaningful growth starts to show around 3–5 years and becomes dramatic after 10+ years thanks to compounding. The key is consistently adding to it rather than leaving just $100 sitting there.

Do I need to pay taxes on my investment gains?

Yes — but it depends on the account type and how long you hold. In a regular brokerage account, gains on investments held over one year are taxed at lower long-term capital gains rates (0%, 15%, or 20% depending on income). In a Roth IRA, qualified withdrawals are completely tax-free — a huge advantage over time.

Your Wealth-Building Journey Starts This Week

You’ve read the guide. You know where to start. The only thing left is to actually do it. Open an account today, invest your first $100, and set up that automatic contribution.

Future you — the one retiring comfortably — is counting on the decision you make this week.

⬇️ Download the Free First Investment Checklist

Free PDF · No email required · 1-page action plan